BIZCHINA> Center

|

BIZCHINA> Center

|

|

Related

Groundwork laid to reform global financial systems

By Wang Xu (China Daily)

Updated: 2008-11-24 09:26

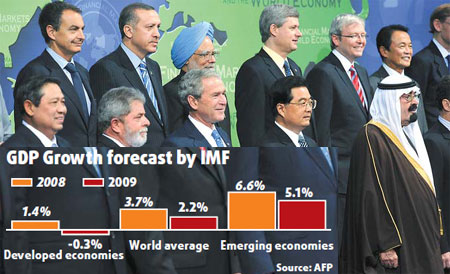

For many skeptics the G20 meeting held in Washington DC on November 15 ended on a surprise note. Despite disagreements, leaders from the 20 major developing and developed economies did lay the groundwork to reform the global financial systems. Though it may take a decade or even longer to fulfill the summit's lengthy to-do list, the leaders managed to set a deadline of next March for tackling the most urgent issues, dismissing the prevailing suspicion that the summit would be nothing but hot air. Far-reaching as its influence might prove to be, some still consider the summit a "damp squib". The leaders' failure to come up with a coordinated stimulus plan, they argue, is wasting the opportunity of giving a much-needed shot to the ailing world economy. "Convening the G20 instead of the G7 is a big achievement in itself, because of the recognition that the world is no longer only US, European and Japanese economies and we need to prepare for future institutional setting, where there are new emerging powers," says Albert Keidel, a senior fellow with Carnegie Endowment for International Peace, a Washington think-tank. "But in terms of pre-empting the real serious downturn that we face today, it (the summit) is a failure." Revamp the system Since the current financial crisis is largely seen as the failure of the regulatory systems, the G20 statement contributed considerable length for reforms in financial rules and regulatory systems. The heads of the 20 States agreed to strengthen regulation from banks' capital to credit-rating agencies. Meanwhile, they also plan to establish colleges of financial supervisors, which will oversee the biggest cross-border financial institutions. Also, a single global accounting procedure will be developed in the next few years, so as to let investors know the true value of their financial assets. The G20 leaders also pledged to reject protectionism and refrain from raising new trade and investment barriers over the coming year, while striving for a successful conclusion of the WTO Doha round of trade talks. For major emerging economies such as Brazil, Russia, India and China, the summit is also a strong recognition of their ascent in economic power. This was the first time that the leaders of all these rich and emerging economies - which represent almost 90 percent of global GDP - had gathered for an economic summit. According to the summit's communique, major international financial institutions, including the World Bank and International Monetary Fund, will be reformed to "reflect changing economic weights in the world economy". And emerging and developing economies should have greater voice and representation in international financial institutions such as the International Monetary Fund and the World Bank. "The meeting is important because it changes the logic of policy decisions," Brazilian President Luiz Inacio Lula da Silvain said in his weekly radio address. "It's no longer the G8, now the G20 has an important role." India's Prime Minister Manmohan Singh referred later to "a clear indication that the balance of power is shifting in favor of emerging economies." Despite the enthusiasm of the new kids in the financial block, the communique of the summit didn't detail how and when the US and Europe will cede their financial power to the late-boomers. "The statement avoided the potentially contentious issue of expanding the IMF's financing capability via recapitalization," says Larry Hatheway, chief economist of UBS Securities. "Many European countries, in particular, are wary of any restructuring of the IMF and added participation by larger emerging economies, as that could well lead to a dilution of European voting rights and potential loss of influence." Unlike India and Brazil, China appeared to be less impressed by the rhetoric, despite the British Prime Minister Gordon Brown's suggestion that China use its foreign exchange reserve to help strengthen IMF's war chest. In his address at the summit, President Hu Jintao echoed the call to advance reform of international financial institutions. However, he also mentioned it's necessary to encourage regional financial cooperation and to enhance the role of a regional assistance funding mechanism, which was left out of the summit's communiqu. "The IMF has been talking about adjusting representation in the fund for years, but progress has been really slow, "says Wing Thye Woo, a senior fellow at Brookings Institution and economics professor from University of California, Davis. "So China could either wait for the real change in a fund dominated by Europe and the US, or help boost the capacity of a fund it already has a say." Finance ministry and central bank officials from 13 Asian nations agreed on November 20 to double the $80 billion pool of currency swaps to safeguard regional financial stability, Philippine Finance Undersecretary, Gil Beltran, said after a meeting in Manila. China, South Korea, Japan and 10 other East Asian nations are launching a $80 billion fund next year. The fund was originally a currency swap pool created after the 1997 Asian financial crisis, after complaints from some Asian nations that the IMF's bailout terms were too stringent. The three East Asian nations will contribute 80 percent of the total fund, or $64 billion, with the other 10 countries chipping in the balance. "Competition to the IMF can be good for borrowers as well as contributors," says Woo. Call for help Although G20 leaders agreed to work on pro-growth economic policies and use monetary and fiscal measures to maintain the growth momentum, observers are disappointed as there is no global stimulus plan coming to their rescue. "A major disappointment of the meeting is the failure to achieve a concerted stimulus package among the G20 nations," said Woo. "The talk about the reform is like trying to come up with a better design of the Titanic upon its collision, rather than getting the sinking people out of the water." Many economists have been pointing at a fiscal stimulus as one of the numbered cures to counteract the current economic slowdown. Major economies such as the US have already lowered the interest rates substantially, but spooked lenders are extremely unwilling to lend at the moment, making it impossible to revive private consumption and corporate investment. "The fiscal stimulus is now essential to restore global growth," IMF's Managing Director Dominique Strauss-Kahn said in a press conference held in the Fund's headquarters on the 15th. "And each country's fiscal stimulus can be twice as effective in raising domestic output growth if its major trading partners also have a stimulus package." He estimates that it needs a large global stimulus, in the order of 2 percent of world GDP, to make a sizeable difference to global growth prospects. "But more countries should join in, not only for the sake of size," says Woo. "If only one country moves to spur domestic demand, it would lead to stronger imports while its exports would stay flat. And it risks running a trade deficit, which will in turn make the stimulus package more difficult." "For China, a decline of trade surplus is not a big issue at the moment. But for those already running a deficit and with only a small foreign exchange reserve, such a single-handed stimulus can last long."

(For more biz stories, please visit Industries)

|