Indicators send confusing growth signals

(China Daily) Updated: 2014-10-21 07:17

Goldman Sachs Group Inc, Global Macro Research

Falling consumer-and producer-price inflation will push up real interest rates, if the nominal interest rate does not fall. This is a key reason why the open market operations rate and interbank interest rate have been falling in recent weeks. We expect policy rates to stay low until the end of the year. The likelihood of other policy loosening, such as interest rate and reserve requirement ratio cuts, has risen. But if these moves do occur, they are likely to come in targeted form as opposed to across-the-board cuts.

Wang Tao, head of China Economics Research at UBS Investment Bank

The People's Bank of China has recently relaxed property lending policies and encouraged banks to increase credit support for the property sector, which may feed through to improved market transactions and stronger demand for property loans in October and November.

Nevertheless, we think such policies can mitigate but not reverse the property sector's structural downshift, and we expect a further slowdown in construction in the fourth quarter onwards. That will exert an increasingly negative drag on other industries.

We expect the central bank to maintain a relatively supportive credit environment to defend the nation's GDP growth target. Further relaxation of credit supply through increased base money supply and relaxation of loan quotas could help, though we do not expect reserve requirement ratio cut soon - unless there are persistent, large foreign-exchange outflows.

We also expect a wholesale cut in benchmark lending rates by the end of 2014 or early 2015 at the latest, to help more effectively in lowering borrowing costs and boosting businesses' cash flow. To support monetary policy and credit demand, however, we also expect the government to launch new infrastructure projects and relax property policies further.

Qu Hongbin, chief China economist at HSBC Holdings Plc

Overall, lending and credit growth remained relatively stable in September. This should help support economic activity in the next few months. However, overall demand conditions remain weak, as indicated by falling inflation and slow de-stocking. This means the economy is operating with a lot of spare capacity. We expect policymakers to introduce more easing measures in the coming months.

As we have been noting for a while, non-bank lending credit activity has been contracting. This continued in September. After taking out bond issuance, the so-called shadow banking part of the system did not extend any new credit in September. Tighter regulation is good for reducing financial risks in the long term, but the near-term impact on system-wide credit needs to be offset by stronger bank lending.

Zhu Haibin, chief China economist at JPMorgan Chase &Co

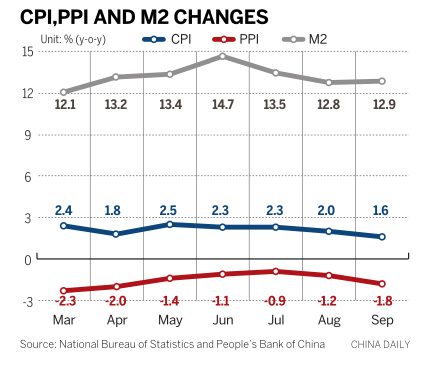

CPI inflation averaged 2.2 percent from a year ago in the first three quarters of 2014, well below the government's full-year target of 3.5 percent. CPI inflation will likely stay modest in the coming months. Our forecast pencils in 2.1 percent for the full year. This provides room for policymakers to focus on growth stabilization and structural reforms in the near term.

The return and deepening of PPI deflation is worrisome. For the overall economy, the industrial pricing environment is closely linked to industrial profits, which in turn have a significant impact on manufacturing investment growth. If the PPI remains subdued going ahead, it would reduce the prospect of a potential near-term recovery in manufacturing fixed-asset investment.

We expect policy rates will stay unchanged and credit growth will remain stable in the coming months. The central bank is reluctant to implement traditional monetary easing, because it is concerned about distortions in the monetary policy transmission mechanism. Instead, a new operational framework may focus on lowering market interest rates; targeted quantitative measures and a shift in credit components to improve direct support from credit to the real sector.

Tang Jianwei, senior economist with Bank of Communications Co Ltd

Although the CPI rise eased to a nearly-five year low of 1.6 percent in September, it generally fell within our expectation. A main reason for the slowdown is eased tail-raising factor.

The trend in the PPI is more worrisome. The drop last month was the 31st consecutive monthly decline, and it was even larger than that of previous two months.

The latest rhetoric of the central bank showed that it remains cautious about "across-the-board easing". Instead, "targeted easing toward selected sectors" will remain the primary method.

Imports grew 7 percent year-on-year, suggesting strong domestic demand that is seemingly at odds with what the CPI indicated.

As the six-year low of industrial output growth in August suggests, domestic demand remains quite weak.

- Economist: Property oversupply to be digested at most within 2 years

- Nomura sees business opportunities in CPC key plenum

- Asia's growth prospects remain solid

- China embraced commodity economy in 1984

- Time for government to continue cracking whip for sustained progress

- Pruning to keep growth on right track

- Powerful future for investment firm

- Slower growth likely in 2015

- Dongfeng Nissan's Dalian plant rolls out cars

- Intangible cultural heritage show opens in East China

- Taking the road less traveled for growth

- Dark Horse offers a bright business idea

- Govt bond yields fall most in one month on stimulus bets

- New strategy for China's big cities

- Speculation grows of early interest rate cut

- Clear message from film app firm