Bailouts have to cover wider spectrum of society

If we thought 2008 was the year of the extraordinary bailouts by Western governments, 2009 may have to become even more extraordinary with governments resorting to lending to a broad spectrum of society - businesses and consumers. Without this, global demand and all that means to China and other developing countries' prospects will remain severely depressed.

We are in danger of becoming immune to the size of individual bailouts for banks, insurers and now the autoindustries. We are also are increasingly expectant that these beneficiaries, like Charles Dickens' Oliver Twist, will "ask for more". There is no clear evidence that these bailouts are working beyond the obvious result that the injection of funds has kept the patients alive.

One sense in which they are not working is that they were injected to deal with the conditions of late last year, but the conditions expected throughout this year are now recognized by most experts and governments to be much worse than last year and much worse than most expected several months ago for this year.

Take the assistance to the autoindustry in the United States and similar assistance in Europe under discussion . The nature of this is that the temporary loans help the players tide through a crisis till the end of the first quarter this year. In theory, during that period, important adjustments can take place.

However, if the auto industry is reeling from like-with-like monthly drops in new car sales of 30 percent or more since last September but with better sales earlier in this year, how much worse must the situation be this year when it is likely that monthly sales drops in the first eight months will continue to be well down on the same months of last year.

The same consumers who decide they can postpone buying a car now because of the economic climate are hardly likely to see a better climate this year.

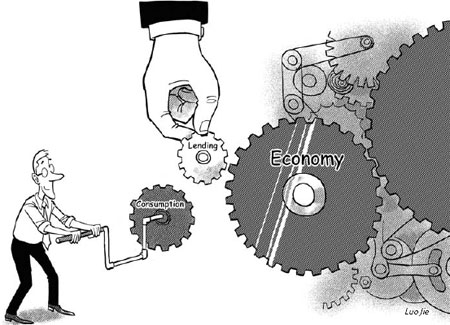

This brings us to a recurring theme. What ultimately matters is the ability of consumers to buy new cars - sure, industry capacity, model range, reliability, fuel efficiency (even at gas below $2 a gallon) come into it - but the key thing is money/credit for car purchase.

That raises the question of how much money should be lent to autocompanies to keep going versus money made available to the consumer to facilitate low-cost car purchase - a spectrum from government grants for purchasing fuel-efficient vehicles to low interest loans and even simply ensuring finance is available.

In the autoindustry this is not too hard to channel to consumers since all the companies have finance arms to provide credit to buyers - assuming these financial companies can access that credit at reasonable rates.

That again brings us back to another aspect of why the bailouts have not yet worked - the main beneficiaries, the banks, have not yet resumed anything like normal lending and certainly not at affordable interest rates. Bank leaders say that credit will remain very tight this year and beyond.

This will hit many businesses as it relates not just to securing additional credit to fund a temporary downturn, but to refinancing a whole load of existing credit coming up for repayment.

This problem is well illustrated by Bank of England data on European companies which shows that this year some $1,000 billion of corporate bonds mature and it will be impossible to raise finance to cover these repayments given the current state of the financial markets. It seems inevitable that governments will have to step in with finance for such company credit.

The banking industry is also unable to provide households with credit on acceptable terms. This is well-illustrated by the ridiculous combination in the US of the Federal Reserves setting a target rate of virtually zero interest in the banking markets, and totally credit-worthy consumers facing hikes in their credit card borrowing rates to triple what they were just a couple of months ago, with rates of 25 percent common and over 30 percent in some cases.

Again, the problems of weak sales, rising unemployment and thus further risks to debt defaults cannot be reversed unless the larger proportion of consumers in Western societies who are still creditworthy can get credit and at the affordable rates that they need.

Western governments have all but used up the "reduction in central bank interest rate tool" as a policy weapon and will have to look in 2009 to more direct methods. In Britain there already exists a social fund to lend at no interest to the most needy - over 1.2 million loans at zero interest were made last year. Discussions on expanding access linking with credit unions are underway. The stumbling block is the need for "partners" to charge interest.

It seems inevitable that governments will have to engage more and more in "social lending" at non-commercial rates if assistance is to reach the members of society that urgently need affordable credit. The alternative of a rapidly rising role for "loan sharks" is unthinkable. So far the commercial banking sector has shown no appetite for this. Perhaps this is not surprising given the loan defaults from risky commercial lending of recent past.

However, the game has changed and responsible social lending is now needed. In some countries this may be achieved by complete nationalization of some banks, in other countries by creating special institutions to channel funds.

But make no mistake, this year with collapsing demand, rocketing unemployment, record bankruptcies matched with severely curtailed credit access and at unaffordable rates is not going to work. Western governments know this, they just need to decide how to fix it. Social lending needs to be on the agenda.

The author is an economist and director of China Programs at the American Institute for Foreign Study

(China Daily 01/06/2009 page9)