Where next for the ChiNext?

Rumors of unrealistic valuations and IPO fraud have seen the high-growth index register a major decline, reports Gao Changxin in Shanghai.

After a grand debut in 2009 and a notable rally last year, the ChiNext board - an exchange for high-growth, high-tech start-ups - has undergone a major retreat this year.

To make matters worse, analysts say the decline of the Shenzhen Stock Exchange's counterpart to the Nasdaq is not due to normal cyclical fluctuation. Rather, they believe that it represents the bursting of a bubble as investors return to rationality.

Worse, the experts have warned that the downward trend could continue, as global and European uncertainties take a toll on the domestic market, especially small-cap companies.

The scale of the retreat has been phenomenal. The ChiNext had shed a third of its value, sliding from a high of 1239.6 on Dec 20 to a record low of 783.86 in intraday trading on June 23.

By comparison, the Shanghai Composite Index, which tracks the bigger of China's stock exchanges, dropped only 5.26 percent from 2825.33 on Jan 1 to 2664.28 on June 16.

Back then, 120, or 54.3 percent, of the 221 stocks on the ChiNext had fallen below their issue price. Among them, 101 stocks were trading at more than 30 percent lower than their debut levels.

The board, which has a lower listing threshold than other indexes, offers riskier but potentially more profitable investment opportunities, and imposes more stringent rules on trading, disclosure of information and delisting.

Unlike investors on the main board, those focusing on the ChiNext often look not at how much the companies are earning at the present time, but at their future growth and potential profitability.

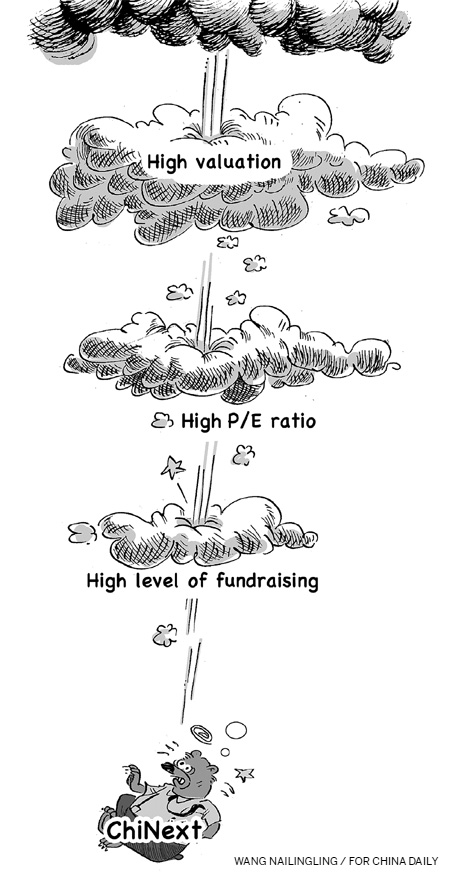

Analysts say that one indication that the board is overvalued is that it has an ultra-high price-to-earnings ratio, a measure of the market's expectation of future earnings growth.

The board's average ratio reached a high of 80.01 this year, before slumping to around 40.

That figure is more than twice that of the A-share market and the New York-based Nasdaq. On June 17, the average price-to-earnings ratio of A-share stocks was 15.76, while the rate for Nasdaq stocks was below 20.

"We have always said that the high price-to-earnings ratio for the ChiNext was unsustainable and a sign of overheating. Now it's been halved to 40, and I think there is further room for adjustment," said Lei Zhonghui, an investment manager with the Zero2IPO Group, a Chinese venture-capital (VC) company.

"The decline in the price-to-earnings ratio is confirmation of our view that many ChiNext stocks are overvalued. The high ratio suggests that the board's companies have great growth potential, which they actually don't," said Lei.

Much of the decline came after investor confidence was dented by the sluggish results reported by the board's companies in the first quarter of this year.

During that period, 23 percent of the 221 ChiNext companies reported a decline in net profit, according to Heading Century Consulting Co Ltd, an IPO consulting firm. And 12 of the 56 companies that have joined the board this year reported a decline in profits.

For example, Xinning Modern Logistics Co Ltd lost 1.81 million yuan ($283,700) in the first quarter, compared with a profit of 2.35 million it registered in the same period a year ago.

Meanwhile, Ningbo GQY Video & Telecom Joint Stock Co Ltd, a maker of video products, saw its first-quarter profit plummet more than 90 percent from 8.51 million yuan in the same period in 2010.

"Investment banks and venture capital firms, which benefit from high issue prices, are behind the board's overvaluation," said Liu Guanwu, an IPO analyst with Analysys International, a Beijing-based consulting firm.

He said investment banks and VC companies will use financial and administrative measures to 'package' companies before their IPOs, in a move to convince investors that a company has great growth potential and deserves a high valuation.

"The higher the issuing price, the higher the commission gained by the investment banks and the return for venture capital, so they have an incentive to push up the issuing prices," Liu said.

For some companies, even the managements themselves seem to have little faith in their company's future, selling their stock immediately after the lock-up period expired.

According to figures from the Shenzhen Stock Exchange, 21 companies on the board were shorted by their own managements in May. And as of May, only 79 ChiNext companies had been listed for longer than the one year lock-up period required before management could sell the stock.

Heading Century said in a recent report that irregularities have been rampant in ChiNext IPOs. Since the board's launch, regulators have received 200 written accusations concerning more than 100 companies, it said.

"The accusations touch on irregularities in equity transfer, affiliated transactions, taxation and patents, exposing the phenomenon that some companies engage in fraud in their IPO processes," Heading Century said in the report.

For now, VC companies, which make a profit out of exits from IPOs, seem to be the biggest beneficiaries of the ChiNext. As of May 30, 134 of the 221 companies on the board were backed by VCs, according to Analysys International.

The board's exceptionally high price-to-earnings ratio, providing exit channels with high returns, has led to a better investment return for VC firms.

The average return on VC/Private Equity investments on the ChiNext stood at 11.59 times, compared with a return of 5.91 times on foreign stock markets, Ni Zhengdong, president of Zero2IPO, told a forum in Shanghai last year.

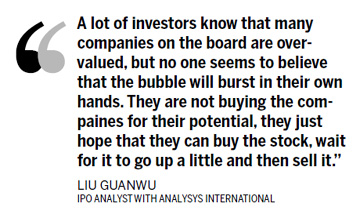

As for investors, Liu said that only a few actually believe that the board's high valuations are reasonable and most of them buy the stock simply for short-term speculation.

"A lot of investors know that many companies on the board are overvalued, but no one seems to believe that the bubble will burst in their own hands," said Liu.

"They are not buying the companies for their potential, they just hope that they can buy the stock, wait for it to go up a little and then sell it."

Zero2IPO's Lei said the timing of the board's launch, when market liquidity was ample and other investment channels were lacking, also helped to prompt investors' passion.

"The sluggish performance of the main board and the government's tightening measures on real estate have narrowed investment channels. And so when the ChiNext came along, many investors thought it would be a good place to put their money," Lei said.

Wang Jianhui, chief economist with Southwest Securities Co Ltd, feels that investors have figured out what the ChiNext really has to offer after witnessing the lower-than-expected results in the first quarter and management selling stock in their own companies.

"The investors have realized that many companies are over-valued and risky, so they will be cautious in the future when investing on the board," he said.

According to Wind Information Co Ltd, a Shanghai-based provider of financial data, 10 of the 26 new stocks on the ChiNext fell below their offer price in first-day trading in May.

In the first 20 days of June, five of the 16 new stocks also stumbled on debut.

"Going forward, the board has further room for adjustment, I think a price-to-earnings ratio of about 30 is a reasonable level for the board," Wang said.

"The price-to-earnings level of 80 won't be seen again in the future, (because) the board has been gradually moving from overheating to rationality."

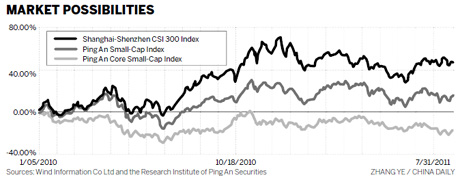

As global economic uncertainties develop, especially in the light of the worsening European sovereign debt crisis, domestic stock markets have become volatile and have dropped continually during recent months.

As a result, the ChiNext dropped by 1.68 percent to close at 829.35 on Monday, after rising to 960.15 in late August from its June low.

China's small-capitalization stocks may extend their declines given the global economic outlook, analysts said. A ChiNext index of start-up companies has tumbled 21 percent this year on concern that monetary tightening will make it more difficult for small companies to borrow from banks and expand businesses.

"Small caps don't weather the downturn as well as their larger counterparts and the outlook for them is very challenging," said Christie Ju, head of Hong Kong and China Research at Jefferies Group Inc.

"China's going to pay for structural changes to its economy as it moves from a model that's export-driven to one more driven by domestic consumption," she said. "This is probably a time that's extremely challenging for the global economy."

Recently, the International Monetary Fund trimmed the estimate for China's year-on-year GDP growth to 9.5 percent this year from 9.6 percent. Meanwhile, the estimate for growth for 2012 was cut to 9 percent from a previous forecast of 9.5 percent in June.

Bloomberg News contributed to this story.

(China Daily 09/28/2011 page14)