New bank rate rules change saving habits

|

An Industrial and Commercial Bank of China Ltd branch office in Beijing. Based on the Basel II and Basel III agreements set by the Basel Committee on Banking Supervision, systemically important banks are required to have a capital adequacy ratio of 11.5 percent by 2018. Provided to China Daily |

Liu Yuqi, 58, a retired teacher, has moved part of her deposits from a major State-owned lender to the Bank of Nanjing for the better interest rate, although her son sneered at her enthusiasm about finding a "tiny" difference.

Like Liu, 1.3 billion Chinese, well known for their saving habits, got different rates to choose from after the central bank in June allowed lenders to price deposits higher than benchmark rates for the first time.

They don't have many alternatives, as prices were divided into two camps - 1.1 times the benchmark offered by joint-stock and smaller lenders, and 1.08 times the benchmark priced by major State-owned banks - but "it can be a good start", Liu said.

A senior executive surnamed Li at the Beijing branch of Bank of China Ltd. acknowledged that the difference in rates is miniscule.

"Most of the depositors are still waiting to see what will happen next because the current difference in rates is too small. For now, we haven't seen a lot of deposit draining," Li said.

The People's Bank of China in June gave lenders permission to set deposit rates up to 1.1 times the benchmark rates.

Thirsty for capital, small and medium-sized lenders set their rates for deposits to the ceiling immediately after the formal announcement went into effect, while major State-owned banks were more conservative, setting the deposit rates at 1.08 times the benchmark rates.

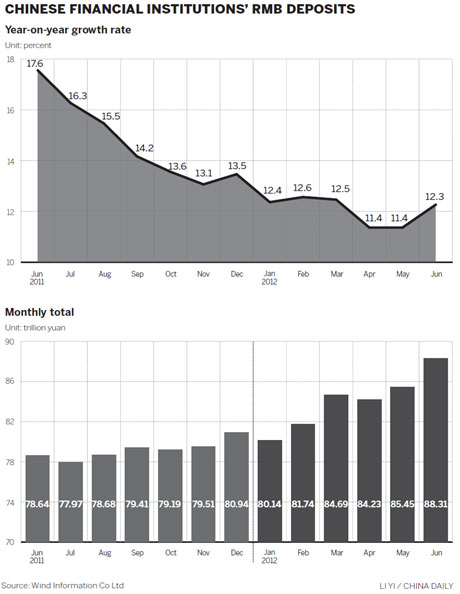

Savings started to drain from banks as wealth management products, funds and trust businesses grew in popularity with depositors. This year, two of the first five months have witnessed year-on-year declines of deposit increases among commercial lenders.

In the first half, outstanding yuan deposits stood at 88 trillion yuan ($13.82 trillion), up by 12.3 percent year-on-year. The pace was 1.2 percentage points lower than six months earlier.

While money paid for deposits increased, banks' interest rates for loans are facing downside pressure as lower limit of lending rates was reduced twice.

Banks were also allowed to set the interest rates charged on their loans at or above 80 percent of the government's benchmark rates, down from the previous 90 percent.

Later in July, the central bank further reduced the lower limit of lending rates to 70 percent of the benchmark rate, but leaving the upper limit of deposit rates untouched.

Li Daokui, a former adviser to the central bank's Monetary Policy Committee and a professor at Tsinghua University, said earlier that more expansion of the allowed range around the benchmark rates will follow.

Morris Li, president of China Guangfa Bank Co Ltd, said the timing of such moves was "very smart", although the liberalization came earlier than expected.

"Freeing rates while cutting them grants a buffer to the lenders as well as clients so that they could have more time to get adjusted," Li said.

Most Chinese banks are scrambling for deposits to meet the China Banking Regulatory Commission rules that require they keep loans to a certain proportion of their respective deposits.

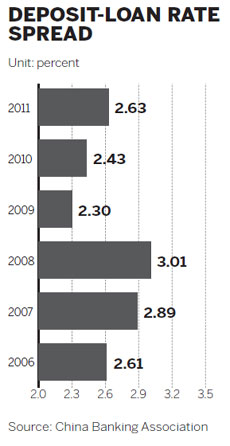

Banks' profits will show "obvious" declines this year as economic growth slows, credit demand softens and net interest margins narrow, said the China Banking Association earlier in July.

The pressure generated from more liberalized interest rates will mainly go to the corporate banking sector. "And surely the spread will continue to fall in the future," Li said.

The banking association said regional small and medium-sized lenders probably cannot stand the crush of a much-narrowed spread, and will become a "short board" for interest-rate liberalization.

For these lenders, credit assets take up more than 80 percent of their total assets, and interest income also accounts for 80 percent of their total income, it said.

As for major banks, credit assets account for 50 to 60 percent of the total assets, while interest income takes up 60 percent of total income.

"This year, it's getting more difficult for small banks like us to collect deposits," said Deng Zhongwu, general manager of the Bank of Sanmenxia in Henan province.

"Our market shares in lending to small enterprises, an area we are concentrating on, have been squeezed by big lenders because they want to adjust their business to counter the narrowing spread due to more market-oriented rates, and show their response to the government's call."

Ma Weihua, president of China Merchants Bank Co Ltd, added: "The liberalization of interest rates is a test of life and death for us."

The lender estimated that if rates become market-oriented, 20 to 30 percent of its clients will have greater bargaining power, which means lending rates to those clients are likely to go down by 15 to 20 percent.

Therefore, it started to restructure its business in 2010, trying to improve the proportion of retail banking and lending to small and medium-sized enterprises to make the effect less once rates were loosened.

But even the "Big Four" State-owned banks are getting increasingly nervous.

Zhang Yun, president of the Agricultural Bank of China Ltd, urged employees at a half-year convention: "In the coming months, we must closely watch market prices, and adjust ABC's pricing and strategy of its liability business in a timely and flexible way."

The State-owned banks' fast reaction and proactive attitude in adjusting prices have shocked smaller lenders and made them even more restless.

Hu Xiaolian, vice-governor of the central bank, said last month that what troubles the authorities most is that promoting rate liberalization will endanger small lenders at the township level and put them on the edge of bankruptcy, which will take tolls on depositors if a deposit insurance system has not yet been established.

"Rising competition would make them raise deposit rates and increase costs. To guarantee enough profit, these lenders will probably charge more for loans - and risks will surge," she said.

By the end of June, 17 regional banks had increased the rates paid on deposits with maturities of more than 2 years to 1.1 times the benchmark rates. Large State-owned lenders applied higher-than-benchmark rates only to 1-year deposits.

After this round of rate hikes, net interest income in the banking industry will evaporate at least 140 billion yuan during the year, said Guo Tianyong, banking research director at the Central University of Finance and Economics.

The government should establish a deposit insurance system to protect depositors' interests and improve the proportion of direct financing to total financing to make the whole market less dependent on regulated interest rates, he said.

At present, lending takes up more than 75 percent of financing in China.

Lu Zhengwei, chief economist at the Industrial Bank Co, said the establishment of a deposit insurance system is not a necessary precondition for a further freeing of rates.

"Such a system means government backup would not exist for most lenders. Fearing a loss of their deposits when rates are freely set, depositors would move their money to State-owned banks because the authorities always underwrite them."

He said a priority should be put on banks to run universal businesses, which is crucial for avoiding the bankruptcy of financial institutions after competition gets fiercer.

Deregulation of the financial market must be put ahead of interest rates and currency liberalization, said Yin Jianfeng, deputy director of the Institute of Finance and Banking at the Chinese Academy of Social Sciences.

"Without sufficient and market-based development of domestic financial institutions, it would be dangerous to free rates first," Yin said.

He said that if banks were unable to develop their business freely when interest rates are liberalized, they will have to spur lending to real estate to guarantee their profits, which will worsen asset bubbles across the country.

But Yang Zaiping, executive vice-president of the banking association, said financial deregulation should not go forward with a "big bang" approach, which would worsen the vicious competition among banks.

"The authorities should give financial institutions sufficient buffer time to adjust their balance and income structure, and to gradually establish a pricing and risk management mechanism," Yang said.

The association said the government should allow Shanghai Interbank Offered Rate, or Shibor, to play a dominant role in determining market interest rates and to make the pricing system more reasonable and orderly.

"But one problem is that most Shibor rates are for one year and cannot reflect middle and long-term rates," it said.

"If Beijing really wants to liberalize rates without causing problems, some supporting policies are needed, such as securitizing bank assets and broadening the definition of capital to alleviate the capital tension of lenders," Li Daokui said.

The State Council has announced new rules that set tougher capital criteria for lenders at the beginning of 2013.

Based on the Basel II and Basel III agreements set by the Basel Committee on Banking Supervision, the tougher standards require what are deemed to be systemically important banks to have a capital adequacy ratio of 11.5 percent.

For banks that are not systemically important, the ratio is 10.5 percent. Banks are expected to meet the requirements by the end of 2018.

Despite the obstacles, many believe freeing rates is "essential" work for China and determines how China's financial industry will be shaped in the future.

"Over the longer term, we believe the liberalization of interest rates will provide the basis for a more efficient allocation of financial resources, and be an important condition in the liberalization of China's capital account," said Ma Jun, chief economist at Deutsche Bank AG in China.

"These fundamental reforms will eventually improve economic performance."

wangxiaotian@chinadaily.com.cn

(China Daily 08/02/2012 page13)