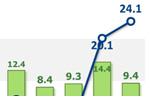

Compared with small and medium-sized enterprises, large State-owned ones and listed companies have had easier access to bank loans. But these loans are sometimes used for repeated arbitrage, resulting in an unhealthy rise in the country's social financing volumes, as indicated by the issuance of a large volume of newly increased lending via non-traditional credit channels.

According to China's central bank, about a half of the country's newly increased credit was lent via "shadow banks". While evading detection from the financial authorities, the unrestricted expansion of shadow banking has not only squeezed the flow of funds to the real economy, it has also increased the financial risks.

Also there can be no denying that the recent liquidity crunch in China is to some extent related to the outflow of some hot money under growing expectations that the United States will withdraw from its years-long quantitative easing.

The Federal Reserve has made clear its intention to phase out its monetary easing policy amid signs of economic recovery. This would have repercussions for the global economy, financial markets and property prices. In this sense, the recent "money crisis" in China is a kind of advance response among investors to such expectations.

The authorities have paid close attention to the problems exposed by the country's money crunch. At a recent State Council meeting, Premier Li Keqiang called on banks to better use their new loans and activate old ones. He also promised more support to economic transformation and upgrading. These messages possibly herald major financial reforms, which are, in fact, inevitable.

The government should continue to tighten its monitoring over liquidity, refrain from recklessly injecting liquidity into the market, rectify the booming non-governmental financing business and change misdistribution of some of its financial resources, in a bid to prompt banks to accelerate their deleveraging, reduce shadow banking activities and channel more financial resources to the real economy.

While maintaining the continuity and stability of the country's monetary policies, the central bank should change its financial regulations from focusing on quantity to focusing on quality and structural optimization.

The country should try to include the opaque shadow banking business into the transparent funds and bonds market, stunt local governments' impulse to expand their leverage-based financing sector and really channel more funds into the real economy to bolster the national economic upgrading.

Efforts should also be made to push for marketized reforms of interest rates in a bid to promote good interaction between the financial sector and real economic players. At the same time, the country should allow non-governmental capital to enter its financial market to promote diversification of its funds supply system.

The author is a professor with the School of Economics and Management at Tongji University in Shanghai.

Models at Ford pavilion at Chengdu Motor Show

Models at Ford pavilion at Chengdu Motor Show

Brilliant future expected for Chinese cinema: interview

Brilliant future expected for Chinese cinema: interview

Chang'an launches Eado XT at Chengdu Motor Show

Chang'an launches Eado XT at Chengdu Motor Show

Hainan Airlines makes maiden flight to Chicago

Hainan Airlines makes maiden flight to Chicago

Highlights of 2013 Chengdu Motor Show

Highlights of 2013 Chengdu Motor Show

New Mercedes E-Class China debut at Chengdu Motor Show

New Mercedes E-Class China debut at Chengdu Motor Show

'Jurassic Park 3D' remains atop Chinese box office

'Jurassic Park 3D' remains atop Chinese box office

Beauty reveals secrets of fashion consultant

Beauty reveals secrets of fashion consultant

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()