|

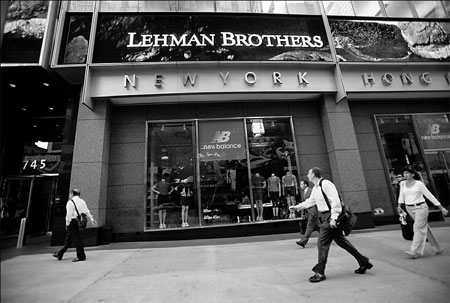

There is a strong consensus on core lessons learned from Lehman's failure and the credit crunch, which forced nations to use over $1 trillion of taxpayer money to rescue banks. Bloomberg News |

LONDON: The collapse of Lehman Brothers a year ago has been likened to the 1994 crash that killed Formula One star Ayrton Senna, in the way it has spurred calls for root-and-branch review of risk in the financial sector.

Senna's tragedy led to regulatory changes in racing that have been effective; deaths on the track are now a rarity.

But governments are not finding it nearly as easy to make quick and comprehensive changes to financial regulation.

That means risks may remain for another collapse on the scale of Lehman in coming years, though authorities would probably be able to act more decisively next time to prevent a financial crisis from spreading around the globe.

The core lesson from Lehman for governments has been clear - regulating against all future crises is futile but there are ways to limit fallout and need for government bailouts.

Britain witnessed at first hand with Lehman the legal nightmare when a complex, global bank goes under. Its financial services minister, Paul Myners, wants banks to simplify their structures and make "living wills".

"We need to move to implementation across the EU. The time has come to move from theorizing to action. Simple structures are an essential precondition for effective arrangements," Myners said.

Patrick Buckingham, a partner at Herbert Smith law firm in London added: "The sheer complexity of the Lehman insolvency has inevitably triggered a desire for a plan for an orderly wind-down in the form of a living will, and may also lead to regulators asking for current entity arrangements to be simplified."

Bankers see the Lehman crash as a major turning point.

"Was Lehman the Senna of international banking? Yes. All the changes to regulation are going to add up to less systemic risk," an investment banking industry official said.

"But are all the lessons learned feeding through into policy changes? Only up to a point," he added.

Leaders of the G20 group of major nations pledged in April this year to strengthen financial supervision.

In the US city of Pittsburgh this month, almost exactly a year after Lehman went bust, they will meet again to reinforce the need for stronger bank capital and wind-up arrangements.

But some of the leaders are openly complaining the reforms are too slow or timid. Talk of a new, commonly adopted framework for financial supervision around the world has fizzled out as governments struggle with the nitty gritty of reaching agreements on regulatory change.

Consensus

There is a strong consensus on core lessons learned from Lehman's failure and the credit crunch, which forced nations to use over $1 trillion of taxpayer money to rescue banks.

The G20 has publicly recognized the need to monitor risk across the financial system, not just within certain markets or at individual institutions. This, as well as moves around the world to make banks hold more capital in reserve, is likely to limit the extent of future crises.

The G20 also wants to regulate credit rating agencies to prevent conflicts of interest from distorting their judgments; supervise hedge funds; and rein in overly generous bonuses for bankers that could encourage wild risk-taking in the markets.

But turning the lessons of Lehman into action is proving difficult, partly because governments appear to be losing their appetite for big, controversial reforms as economies start to revive and change seems less urgent.

The European Union and the United States, for example, plan new bodies to monitor system-wide risks. But EU leaders have insisted the new European Systemic Risk Body can make only non-binding recommendations if it spots a problem, thereby preserving national sovereignty.

In the United States, debate still rages on the exact role of the Federal Reserve in monitoring future risks.

"The American regulatory structure is in total disarray and what has been proposed to fix it is partial, and even then there is heavy resistance," said Hal Scott, Nomura Professor on International Financial Systems at Harvard Law School.

"I don't see us coming out with any significant change to the structure. The right rules and the wrong system is what we might end up with."

Said an official at a major US bank, "Would the new EU risk body be heeded if it said the Spanish housing market is overheated? Would a newly systemic Fed have acted sooner on an asset bubble in the United States?" There are grounds for doubt in both cases as no government wants to kill a boom, he added.

Mechanism

It is also proving hard to implement the G20's pledge to create a mechanism to wind up failing international banks quickly. Countries are quibbling over details of the mechanism partly because they fear it could mean disadvantaging domestic creditors in favor of foreign ones.

Global banks have become very complex as they seek to exploit national differences in tax and regulation so a more harmonized global approach to those two issues is also needed, a tough challenge.

"Everybody is now recognizing that we need a special legal regime for catching banks when they fall over," said Simon Gleeson, a partner at Clifford Chance, a law firm in London.

Reuters

(China Daily 09/14/2009 page11)

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()