CHINA> National

|

CHINA> National

|

|

China's stock markets continue to bleed

(China Daily)

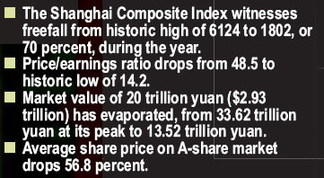

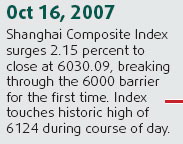

Updated: 2008-10-17 08:00 It was the first anniversary of the benchmark Shanghai Composite Index hitting a historic high of 6124 on Thursday - but there was nothing to celebrate. During the past year, the index has fallen nearly 70 percent, losing market value of 20 trillion yuan ($2.93 trillion). The average share price on the A-share market dropped nearly 60 percent, making almost every investor a loser. And there seems no end to the freefall.

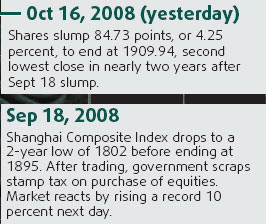

Weighed down by fears over a global recession, the Shanghai bourse fell 4.25 percent Thursday to end at 1909, its second lowest level in nearly two years after the Sept 18 slump to 1895. The Shenzhen Component Index finished at 6167, down 3.74 percent.

Losers outnumbered gainers by 808 to 65 in Shanghai and 697 to 47 in the smaller Shenzhen market. Investor confidence was hit by news of lower corporate earnings. More than half of the 23 companies that had released quarterly reports revealed profit declines in the third quarter.

The market slump came after Wall Street reported the biggest fall in two decades overnight. The Dow Jones industrials plummeted 733 points, or 7.9 percent, it's second-largest point loss ever. Regional markets in Asia mostly fell amid growing fears of a global recession, with Japan plunging more than 11 percent and Hong Kong down 4.8 percent. Following Asia's lead, benchmarks in Britain, Germany and France slipped about 3 percent. European Union leaders meeting for a two-day summit called Thursday for action to preserve growth and jobs and maintain industrial competitiveness as the worst financial crisis for 80 years raised fears of a deep recession.

The 27 leaders said a forthcoming international summit to reform the global financial system should take early decisions on transparency, global standards of regulation, cross-border supervision and an early warning system to restore confidence. French President Nicolas Sarkozy said he and European Commission President Jose Manuel Barroso would meet US President George W. Bush tomorrow to help prepare for a summit that would decide on a "re-foundation of capitalism". Having won the backing of other major economies including the United States for the meeting, EU leaders turned their attention to the likely impact of the credit crunch on their own wider economies.

A Reuters poll of economists Thursday found 34 out of 41 surveyed believe the euro zone is already in recession and most say it will last between six months and a year. In the latest sign that global recession could follow hard on the heels of the credit crisis, new British figures showed unemployment shooting up to 5.7 percent at its fastest pace since a 1991 slump, with experts predicting worse to come. "We are not out of the tunnel yet," said Swedish Prime Minister Fredrik Reinfeldt, urging other EU members to back the measures taken by Britain and the 15 euro zone countries. "Then we have the tools to get out of the tunnel."

"Of course we see that the economic crisis is there, and the question I asked was: If we can bring coordinated answers to the financial crisis, can we not bring a coordinated answer to the economic crisis?" Sarkozy said, pledging that current EU president France would take initiatives on the matter. Switzerland followed the lead of other European countries and the United States Thursday by announcing it would inject billions of dollars into its banking system, chiefly to the benefit of its largest bank UBS. In Asia, Singapore said Thursday it will guarantee $102 billion of foreign currency bank deposits for more than two years after regional finance rival Hong Kong moved to protect its deposits earlier this week. Agencies |