China's trade still in good place despite woes worldwide

By LIU YUANCHUN | China Daily | Updated: 2023-07-10 09:52

Recently, there have been voices of concern over China's trade performance. Indeed, with a discouraging external environment — the global purchasing managers index continues to decline, the trade order index is still in contractionary territory, the currency index continues a downtrend and global investment is declining — it is natural to think in a pessimistic way about the nation's foreign trade, not to mention that some of the leading trade parameters, such as the export delivery index, new orders index and container index, are all telling a similar story.

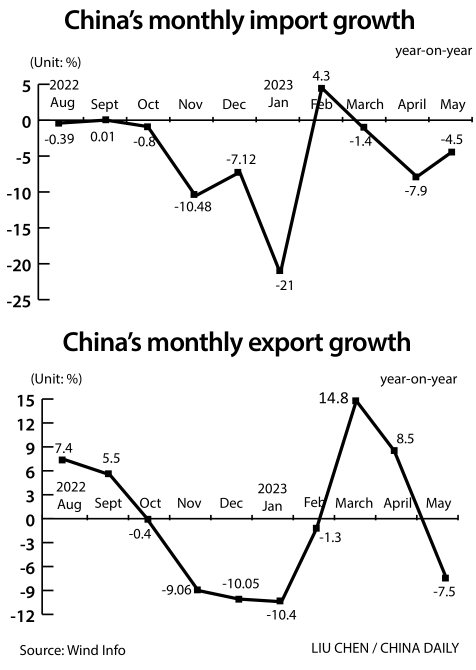

The nation's export growth witnessed consecutive increases in March and April — by 14.8 percent and 8.5 percent year-on-year, respectively, and then shrank 7.5 percent in May, triggering concerns over China's foreign trade vitality.

Such concerns are somewhat overplayed, because trade data fluctuate greatly from month to month. In fact, since 2018, China's foreign trade performance has repeatedly impressed some market observers, especially those who do not clearly understand China's exact trade situation. For example, in 2019, when the Sino-US trade conflict intensified, many were worried that China's foreign trade would be under great pressure. Also, at the beginning of this year, there were fears that the global economic downturn, geopolitical deterioration, coupled with the establishment of US industrial and supply chain alliances and the consolidation of diplomatic alliances, will inevitably make China's external situation deteriorate comprehensively, leading to a further downtrend in China's foreign trade.

However, looking back at the situation over the past three years, it is foreign trade performance that among all major economic drivers has been the most supportive of macroeconomic stability. During this period, the average growth rate of China's trade exceeded 20 percent. So why has China's foreign trade not "collapsed" as many predicted, but bucked the trend and shown a different trend from global trade in general? To arrive at the answers, it requires us to deeply study the changes in China and the global economy, and also carefully analyze how the competitiveness of China's foreign trade has changed in the context of the current great changes.

Recovery pace inconsistent

China's economy is recovering, but unlike recoveries seen in the past, the current one is fundamentally different from previous cyclical rebounds, and this difference comes from the superposition of three main forces. It is a recovery seen after the ravage of the three-year COVID-19 pandemic, a recovery following some of the largest and most thorough adjustments of the nation's real estate sector since its reform and opening-up began, and a recovery at a time when momentous changes that haven't been seen in decades are accelerating and the global economic landscape takes on a totally new look.

Economic recoveries after pandemics like COVID-19 are normally phased and exhibit different characteristics at different stages. Especially in the transition from repairing social order to rejuvenating economic activity and profitability — and then helping balance sheets resume vitality — some fluctuations and pullbacks in indicators are the norm. Therefore, it is not appropriate to overexplain the pullback of some indicators that many are concerned about, nor should the fluctuations merely be interpreted in the current economic situation as a trend toward another bottom.

China's economy is still in the process of recovery, but the pace is inconsistent. Of course, policy support is still needed in this phase to pave the way.

Trade remains sound

Foreign trade data best reflect the overall economic situation, such as the negative growth in imports over the past few months, which indicates that the nation is facing insufficient domestic demand. China's exports, however, continued to grow, even maintaining a double-digit growth rate, resulting in a sharp rise in the trade surplus. Overall, though there have been worries and anxieties over China's foreign trade, the overall trade situation during the past three years suggests things are still in a good shape. As we see, there are three major reasons behind this.

First, the nation's trade structure is now quite different from what it was a short time ago. Over the past three years, the trade volume between China and the United States has contracted, but the specifics vary from year to year. During US Secretary of State Antony Blinken's visit to China last month, he said that Sino-US trade is still growing. Many expressed surprise as Chinese exports to the US fell 15.1 percent from January to May. But actually, he could also be right if the factor of the denominated currency is taken into consideration. In 2021 and 2022, the trade volume between the two countries did expand, and so did China's trade surplus.

Despite the overall positive growth in trade between China and the European Union, the US has replaced China as the EU's largest trading partner. More importantly, China's trade with Japan and South Korea is also shrinking. In particular, the trade deficit with Japan has contracted sharply, and last year the deficit was almost nonexistent.

China's trade with emerging economies, in contrast, continues to grow. In particular, trade with members of the Association of Southeast Asian Nations has been growing at a rate of more than 20 percent for several years, and the average growth rate from January to May this year was above 15 percent. However, the year-on-year growth rate for May alone was negative, mainly due to last year's high base level — that is why, making conclusions with single-month results is not necessarily informative.

In addition, trade with markets involved in the Belt and Road Initiative, such as Russia and those in South America and Africa, is also on the rise. The nation's trade structure, reflected by the trade situation between itself and developed markets and emerging ones, has changed fundamentally.

Second, the impact of the US' moves to repatriate manufacturing on China's trade may turn out to be limited. To secure its industrial supply chains, the US moved to promote the reshoring of its manufacturing players, friendshoring in India and Southeast Asia for outsourcing, and nearshoring by forming a North American alliance with Canada and Mexico.

This is not the first time that the US has promoted manufacturing reshoring, as in the 1980s, it also happened while it was struggling with a surge in Japanese imports. But due to the power of the free market, the outcome turned out to be less impactful than anticipated. Also, while the US has been in full swing to promote friendshoring and nearshoring, trade between the countries it outsources from and China has also skyrocketed. For example, in 2021, China's trade with Mexico surged. That is because the very first step for Mexico to become a manufacturing base is to have a large number of machinery and equipment assets, which China can produce competitively at the lowest cost. At the same time, to industrialize its production line, energy is a must. Mexico has to introduce a lot of power generation equipment to this end, and meanwhile also meet the green power requirements of the US by seeking photovoltaic solutions from China.

Third, China has made breakthroughs in high-tech industries, especially in the emerging sectors. In the first five months, combined exports of lithium batteries, photovoltaic equipment and new energy vehicles increased by 66.9 percent year-on-year, directly driving overall export growth by 2.1 percentage points. China has become a major power in advancing the development of new technology and industries, forming new growth points for itself and enhancing its competitiveness.

Future outlook

Being the world's largest car producer and exporter, China has unavoidably squeezed other major car exporters in the global auto sector, such as South Korea and Japan. This in turn further led to a sharp contraction of China's trade deficit with these countries.

So the external environment is getting more complicated and harsh, but this does not necessarily bring us adverse effects. In some cases, it represents opportunities for China to consolidate its foundation and promote the continuous prosperity of its emerging industries.

For example, amid the global stagflation, China has cost advantages brought about by its large-scale manufacturing sector, which is one solution to stagflation. Also, the decline in global commodity prices, for a commodity-importing country like China, can help further reduce production costs.

In addition, to ensure the security of its own industrial and supply chains, countries are shortening their industrial chains. They will have to make corresponding layouts accordingly, which leaves China a new window period. The nation's efforts in building a unified domestic market will also serve as a platform for high-tech players to sharpen their competitive edge.

To sum up, opportunities and challenges coexist in the path going forward, and to tap these opportunities and overcome challenges, confidence will be key.

The writer is president of the Shanghai University of Finance and Economics. This op-ed is a translation of the writer's speech to a forum organized by the China Macroeconomy Forum, a think tank, in June.

The views don't necessarily reflect those of China Daily.

Related Stories

Editor's Pick